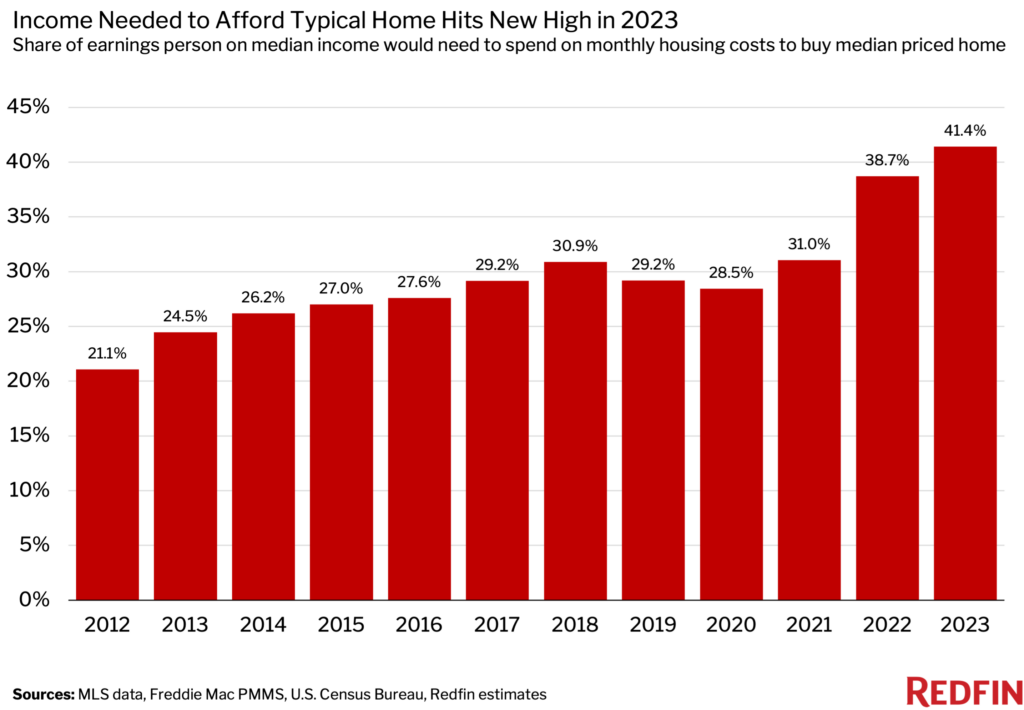

- A homebuyer with the median U.S. income would’ve had to spend a record 41% of earnings on monthly housing costs in 2023, up from 39% in 2022 and 31% in 2021.

- The least affordable markets were Anaheim and San Francisco, where homebuyers with the typical local income would’ve needed to spend over 80% of their pay on monthly housing costs. Detroit and Pittsburgh were the most affordable.

- Austin was the only market that was more affordable for homebuyers in 2023 than in 2022.

- Affordability should improve in 2024 as home prices and mortgage rates tick down.

2023 has been the least affordable year to buy a home in Redfin’s records, but things are looking up for 2024.

Someone making the $78,642 median U.S. income in 2023 would’ve had to spend 41.4% of their earnings on monthly housing costs if they bought the $408,806 median-priced U.S. home. That’s the highest share on record and is up from 38.7% in 2022.

That’s according to a Redfin analysis that estimates monthly housing payments for the typical homebuyer using median home sale prices, monthly mortgage rates (averaging 6.73% for 2023) and median household incomes, and the assumption of a 20% down payment, principal, interest, taxes and insurance. To estimate 2023 median household incomes, we multiplied the available 2022 income data by the 2023 wage growth rate. Data for 2023 goes through October, while data from past years spans the full year. When we refer to a record high, we are referencing records dating back to 2012.

A rule of thumb in personal finance is that people should spend no more than 30% of their income on housing, but that has become less realistic due to elevated mortgage rates and home prices.

The typical 2023 homebuyer needed to earn an annual income of at least $109,868 if they wanted to spend no more than 30% of their earnings on monthly housing payments for the median-priced home. That’s a record high—up 8.5% from 2022—and is $31,226 more than the typical household makes in a year.

“A perfect storm of inflation, high prices, soaring mortgage rates and low housing supply caused 2023 to go down as the least affordable year for housing in recent history,” said Redfin Senior Economist Elijah de la Campa. “The good news is that affordability is already improving heading into the new year. Mortgage rates are coming down, more people are listing homes for sale, and there are still plenty of sidelined buyers ready to take a bite of the fresh inventory. We expect these conditions to continue to improve in 2024.”

Homebuyers’ monthly payments have grown more than twice as fast as wages

Housing affordability has dwindled because wages haven’t increased as quickly as homebuying costs. The median monthly housing payment for homebuyers in 2023 was a record $2,715, up 12.6% from 2022. Over the same period, the median household income rose just 5.2% to an estimated $78,642—also a record high, but not high enough to offset the jump in housing costs.

Monthly mortgage costs for homebuyers soared this year as the Federal Reserve raised interest rates to combat inflation. The average 30-year-fixed mortgage rate hit a 23-year high of 7.79% in October, and while it has since fallen to 7.22%, that’s still more than double the 2.65% record low hit during the pandemic.

Elevated mortgage rates have cooled homebuyer demand, but housing prices remain high because there aren’t enough homes for sale. The $408,806 median home sale price in 2023 is the highest of any year on record. Many homeowners are opting to stay put because selling and buying a new home would mean losing their low mortgage rate.

Austin is the only metro that became more affordable; Anaheim and Miami saw the biggest decreases in affordability

In Austin, TX, someone making the $99,523 median income in 2023 would have had to spend 36.6% of their earnings on monthly housing costs if they bought the $456,950 median-priced home, down from 37.7% in 2022. That’s the only decline among the 50 most populous U.S. metropolitan areas.

The smallest increases were in Detroit (+0.7 ppts to 18.5%), Oakland, CA (+0.7 ppts to 53.3%), Phoenix (+0.9 ppts to 40.2%) and Las Vegas (+1.2 ppts to 43.8%).

Most of these places have something in common: Affordability can’t get much worse because it has already become so strained. Austin, Phoenix and Las Vegas exploded in popularity during the pandemic as remote workers flocked in, causing home prices to skyrocket. With so many people now priced out, costs have started coming back down to earth. Austin posted a bigger home price decline than any other major metro this year (-9.2% YoY). It is followed by Oakland (-5%), Phoenix (-4.1%) and Las Vegas (-3.6%).

In Anaheim, CA, someone making the $92,306 median income in 2023 would’ve had to spend 88.3% of their earnings on monthly housing costs if they bought the $1,022,075 median-priced home, up from 80.2% in 2022. That’s the biggest jump among the 50 most populous metros. Next came Miami (+7.1 ppts to 54.1%), West Palm Beach, FL (+6.2 ppts to 49.1%), San Diego (+5.9 ppts to 64.6%) and Newark, NJ (+5.6 ppts to 42.8%).

Many of those metros have something in common: Home prices are still rising because there’s still demand from buyers who are coming in from more expensive areas to get more bang for their buck. Miami and West Palm Beach are also attracting out-of-staters who prefer Florida’s low taxes, warm weather and politics. Miami posted the second biggest increase in home prices among the 50 most populous metros this year, up 8.2% from 2022 (Milwaukee came first). It is followed by Newark (+8.2%) and West Palm Beach (+7.6%).

California dominates list of least affordable metros; midwest metros rank among most affordable

In Anaheim, someone making the median income in 2023 would’ve had to spend 88.3% of their earnings on monthly housing costs if they bought the median priced home—the highest share among the 50 most populous metros. Next come four other expensive California metros: San Francisco (85.4%), San Jose, CA (73%), Los Angeles (72.9%) and San Diego (64.6%).

Most people who make the median income in these areas are forced to rent because it’s not financially feasible to get a mortgage if your monthly payment represents 70% or 80% of your monthly income.

At the other end of the spectrum is Detroit, where someone making the median income in 2023 would’ve had to spend 18.5% of their earnings on monthly housing costs if they bought the median priced home—the lowest share among the metros Redfin analyzed. It’s followed by Pittsburgh (23.5%), Cleveland (23.8%), Philadelphia (23.9%) and St. Louis (25.2%). These five metros have lower median home sale prices than anywhere else in the nation—all below $300,000.

Hope for 2024: Mortgage payments fall, housing supply rises

Housing costs have started to decline as mortgage rates have fallen; the typical homebuyer’s monthly payment was $2,575 during the four weeks ending November 26, down from its peak last month but still up 13% year over year. New listings posted the biggest annual uptick in more than two years.

In 2024, Redfin predicts listings will climb further, mortgage rates will fall to about 6.6%, and prices will drop 1%.

Metro-level summary: 2023

Table below includes 50 most populous U.S. metropolitan areas; 2023 data covers Jan. 1-Oct. 31 and year-over-year changes compare with the full year of 2022. Median incomes are relative to each metro.

| U.S. metro area | Share of earnings someone on median income would’ve had to spend on monthly housing costs to buy median priced home | YoY change in share of earnings someone on median income would’ve had to spend on monthly housing costs to buy median priced home | Median monthly housing payment for homebuyers | Median estimated household income | Median home sale price | YoY change in median home sale price |

|---|---|---|---|---|---|---|

| Anaheim, CA | 88.3% | 8.1 ppts | $6,794 | $92,306 | $1,022,075 | 3.1% |

| Atlanta, GA | 34.2% | 2.6 ppts | $2,542 | $89,290 | $382,673 | 1.7% |

| Austin, TX | 36.6% | -1.2 ppts | $3,033 | $99,523 | $456,950 | -9.2% |

| Baltimore, MD | 30.0% | 2.7 ppts | $2,381 | $95,211 | $358,335 | 3.1% |

| Boston, MA | 49.3% | 4.9 ppts | $4,503 | $109,723 | $677,695 | 4.4% |

| Charlotte, NC | 38.2% | 2.4 ppts | $2,586 | $81,166 | $389,373 | 0.3% |

| Chicago, IL | 29.1% | 2.6 ppts | $2,116 | $87,226 | $318,578 | 3.1% |

| Cincinnati, OH | 27.3% | 3.4 ppts | $1,796 | $78,965 | $270,280 | 7.3% |

| Cleveland, OH | 23.8% | 1.9 ppts | $1,362 | $68,588 | $204,773 | 2.4% |

| Columbus, OH | 32.2% | 3.6 ppts | $2,136 | $79,717 | $321,500 | 6.0% |

| Dallas, TX | 38.5% | 2.1 ppts | $2,794 | $87,130 | $420,845 | -0.5% |

| Denver, CO | 44.0% | 2.2 ppts | $3,815 | $104,122 | $574,500 | -1.2% |

| Detroit, MI | 18.5% | 0.7 ppts | $1,155 | $74,971 | $173,785 | -2.6% |

| Fort Lauderdale, FL | 44.1% | 5.3 ppts | $2,734 | $74,449 | $411,700 | 6.9% |

| Fort Worth, TX | 32.5% | 1.2 ppts | $2,359 | $87,130 | $355,359 | -2.2% |

| Houston, TX | 33.5% | 1.6 ppts | $2,199 | $78,756 | $331,251 | -1.2% |

| Indianapolis, IN | 29.0% | 3.0 ppts | $1,929 | $79,767 | $290,462 | 5.2% |

| Jacksonville, FL | 35.0% | 1.9 ppts | $2,380 | $81,617 | $358,481 | -0.6% |

| Kansas City, MO | 31.2% | 2.9 ppts | $2,059 | $79,195 | $309,900 | 3.7% |

| Las Vegas, NV | 43.8% | 1.2 ppts | $2,718 | $74,478 | $409,237 | -3.6% |

| Los Angeles, CA | 72.9% | 3.9 ppts | $5,611 | $92,306 | $844,500 | -1.0% |

| Miami, FL | 54.1% | 7.1 ppts | $3,354 | $74,449 | $504,990 | 8.2% |

| Milwaukee, WI | 32.0% | 4.3 ppts | $1,989 | $74,585 | $299,300 | 9.0% |

| Minneapolis, MN | 30.4% | 2.2 ppts | $2,433 | $96,091 | $366,350 | 1.3% |

| Montgomery County, PA | 39.8% | 4.3 ppts | $2,935 | $88,497 | $441,671 | 5.5% |

| Nashville, TN | 41.7% | 2.3 ppts | $2,928 | $84,196 | $440,981 | -0.4% |

| Nassau County, NY | 50.9% | 3.7 ppts | $4,084 | $96,323 | $614,355 | 1.2% |

| New Brunswick, NJ | 39.7% | 4.5 ppts | $3,191 | $96,323 | $479,854 | 6.0% |

| New York, NY | 56.7% | 3.7 ppts | $4,548 | $96,323 | $684,750 | 0.5% |

| Newark, NJ | 42.8% | 5.6 ppts | $3,434 | $96,323 | $516,500 | 8.2% |

| Oakland, CA | 53.3% | 0.7 ppts | $5,983 | $134,815 | $900,575 | -5.0% |

| Orlando, FL | 41.7% | 3.5 ppts | $2,627 | $75,594 | $395,722 | 2.9% |

| Philadelphia, PA | 23.9% | 1.2 ppts | $1,761 | $88,497 | $265,100 | -1.0% |

| Phoenix, AZ | 40.2% | 0.9 ppts | $2,924 | $87,194 | $440,266 | -4.1% |

| Pittsburgh, PA | 23.5% | 1.7 ppts | $1,456 | $74,279 | $218,973 | 1.5% |

| Portland, OR | 45.6% | 2.3 ppts | $3,571 | $93,956 | $537,783 | -1.1% |

| Providence, RI | 40.1% | 4.5 ppts | $2,872 | $86,037 | $432,225 | 6.0% |

| Riverside, CA | 49.8% | 2.8 ppts | $3,615 | $87,109 | $544,375 | -0.7% |

| Sacramento, CA | 47.5% | 2.0 ppts | $3,714 | $93,877 | $558,975 | -2.2% |

| San Antonio, TX | 33.7% | 1.3 ppts | $2,085 | $74,206 | $314,048 | -2.1% |

| San Diego, CA | 64.6% | 5.9 ppts | $5,604 | $104,072 | $843,450 | 3.2% |

| San Francisco, CA | 85.4% | 2.4 ppts | $9,597 | $134,815 | $1,444,700 | -3.5% |

| San Jose, CA | 73.0% | 5.1 ppts | $9,528 | $156,643 | $1,433,625 | 0.7% |

| Seattle, WA | 54.3% | 2.6 ppts | $5,086 | $112,468 | $765,760 | -1.4% |

| St. Louis, MO | 25.2% | 2.4 ppts | $1,647 | $78,407 | $247,852 | 4.1% |

| Tampa, FL | 40.6% | 2.4 ppts | $2,464 | $72,893 | $371,024 | 0.1% |

| Virginia Beach, VA | 33.5% | 3.6 ppts | $2,188 | $78,433 | $329,340 | 5.5% |

| Warren, MI | 30.5% | 3.0 ppts | $1,904 | $74,971 | $286,465 | 4.2% |

| Washington, DC | 34.2% | 2.9 ppts | $3,521 | $123,538 | $530,375 | 2.6% |

| West Palm Beach, FL | 49.1% | 6.2 ppts | $3,047 | $74,449 | $458,807 | 7.6% |

| National—U.S.A. | 41.4% | 2.7 ppts | $2,715 | $78,642 | $408,806 | 0.5% |

United States

United States Canada

Canada