Mortgage applications and Redfin’s demand index, a measure of tours and other homebuying services, are up as mortgage rates continue to come down. But pending home sales declined and the number of homes on the market increased as buyers took a break over Thanksgiving.

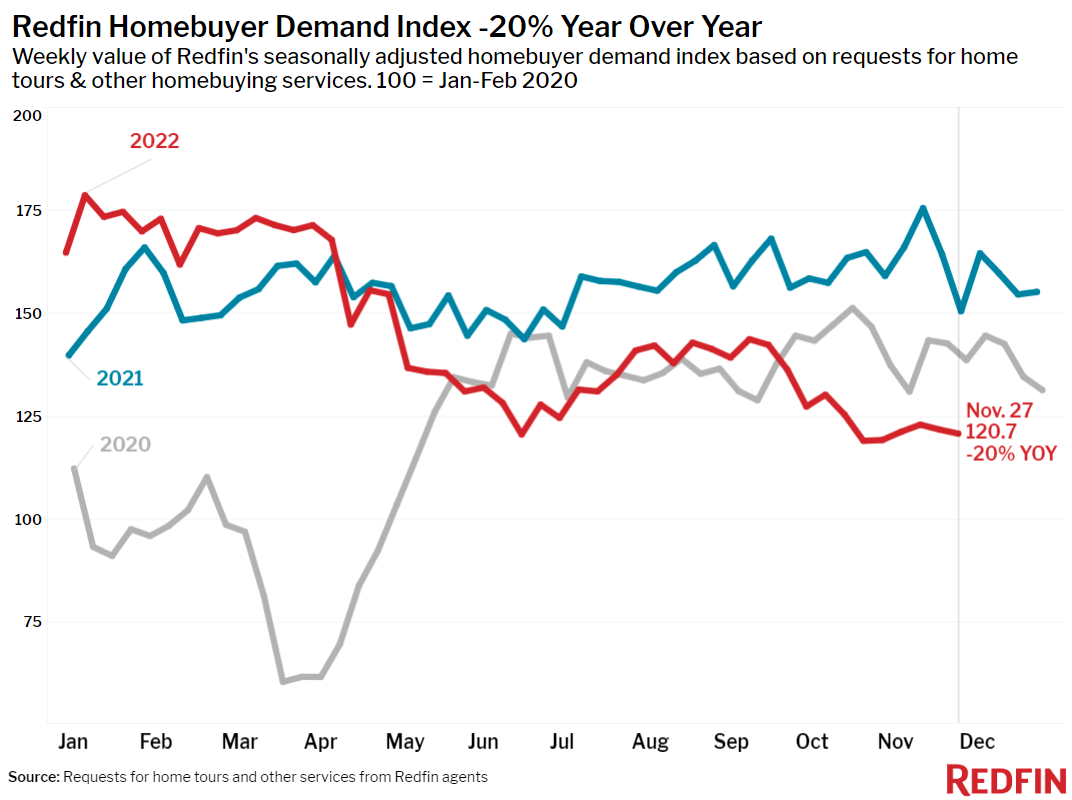

Homebuying demand has started ticking up as mortgage rates continue their steady decline. Daily rates dipped to 6.29% on December 1, down one full percentage point from a peak of 7.29%, hit one month earlier. Mortgage-purchase applications are up 4% from a week ago and Redfin’s Homebuyer Demand Index is up about 1.5% from a month ago.

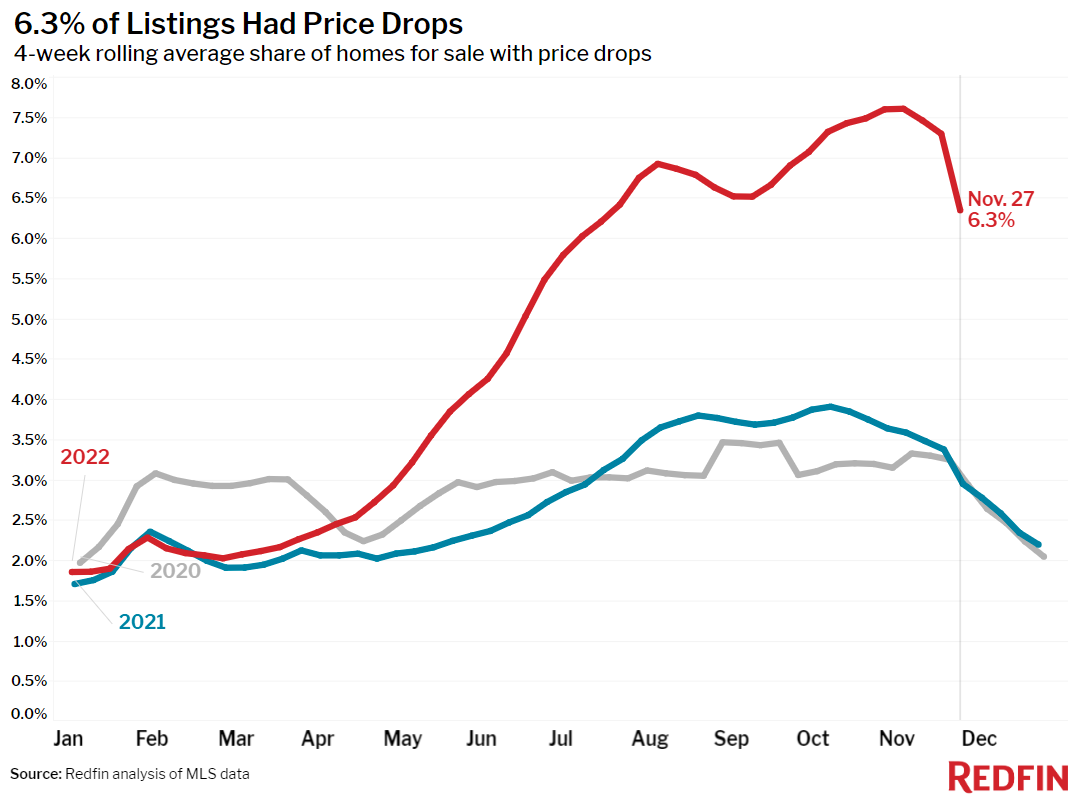

Price drops are becoming less common now that mortgage rates in the 6.5% range are thawing still-cool homebuyer demand. Just over 6% of homes for sale each week during the four weeks ending November 27 on average had a price drop, down sharply from 7.2% a week earlier and the lowest level since July.

“There have been a handful of pieces of relatively good news for the housing market lately, but we’re far from out of the woods. Key indicators of homebuying demand will likely be teetering on a knife’s edge with every data release that comes out related to the Fed’s path to eventually bringing rates down,” said Redfin Deputy Chief Economist Taylor Marr. “We’re likely past peak inflation, past peak mortgage rates and past the bottom for mortgage purchase applications. But there’s further cooling ahead for the housing market, as sales and prices have further to fall before buyers and sellers become comfortable with homebuying costs again.”

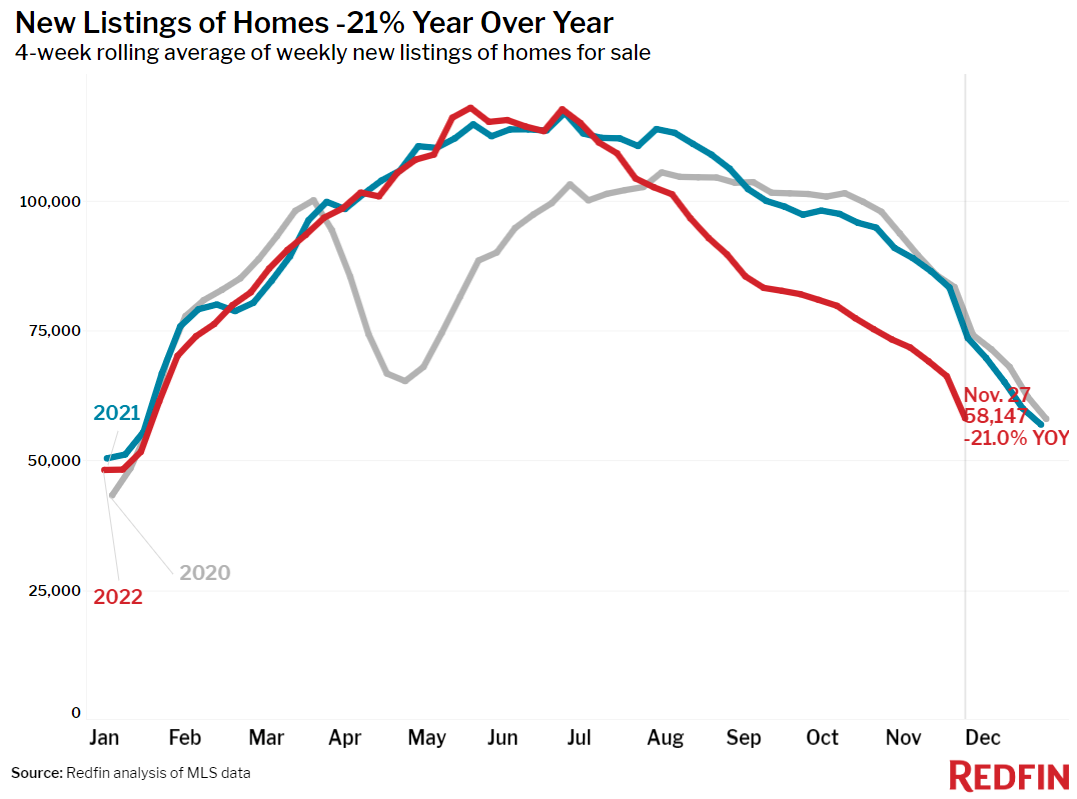

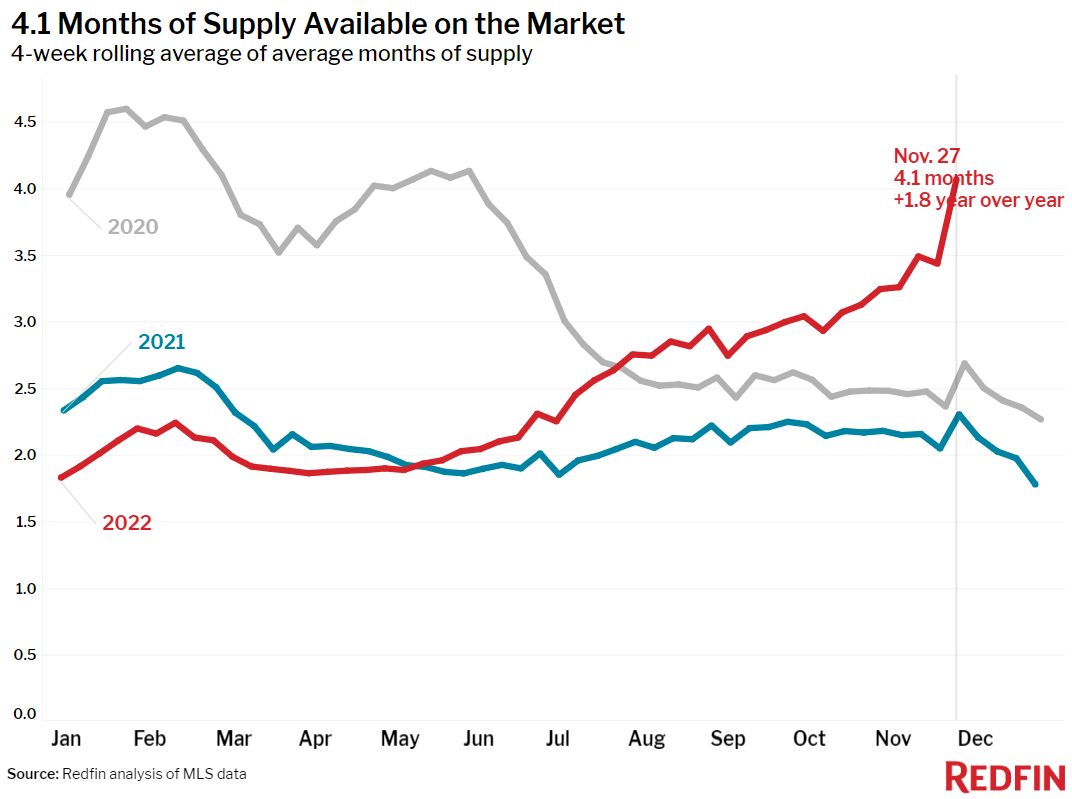

Months of supply–a measure of the balance between supply and demand, calculated by dividing the number of active listings by closed sales–hit 4.1 months during the four weeks ending November 27, up sharply from the prior four-week period and the highest level since May 2020. The supply of homes for sale posted its biggest year-over-year increase on record even as new listings declined by double digits, indicating homes lingered on the market over Thanksgiving week.

Home prices are falling from a year earlier in 10 of the 50 most populous U.S. metros

Among the 50 most populous U.S. metros, home-sale prices fell from a year earlier in 10 of them. Prices fell 8.2% year over year in San Francisco, 2.8% in San Jose, CA, 2.7% in Pittsburgh, 2.3% in Detroit, 1.7% in Sacramento and 1.3% in Austin. They declined less than 1% in Chicago, San Diego, Los Angeles and Philadelphia.

This marks the first time Austin and Los Angeles home prices have fallen on a year-over-year basis since mid-2019. It’s the first time Chicago prices have fallen since June 2020.

Leading indicators of homebuying activity:

- For the week ending December 1, 30-year mortgage rates ticked down to 6.49%. The daily average dipped to 6.29% on December 1, down one full percentage point from the peak of 7.29% reached on November 4.

- Mortgage purchase applications during the week ending November 25 increased 4% from a week earlier, seasonally adjusted for Thanksgiving effects. Purchase applications were down 41% from a year earlier.

- Fewer people searched for “homes for sale” on Google than this time in 2021. Searches during the week ending November 26 were down about 40% from a year earlier.

- The seasonally adjusted Redfin Homebuyer Demand Index–a measure of requests for home tours and other homebuying services from Redfin agents–was up 1.5% from a month earlier but down 20% from a year earlier during the four weeks ending November 27.

- Touring activity as of November 27 was down 53% from the start of the year, compared to a 37% decrease at the same time last year, according to home tour technology company ShowingTime. Touring activity declined less during this year’s Thanksgiving week than it has in past years.

Key housing market takeaways for 400+ U.S. metro areas:

Unless otherwise noted, the data in this report covers the four-week period ending November 27. Redfin’s weekly housing market data goes back through 2015.

Data based on homes listed and/or sold during the period:

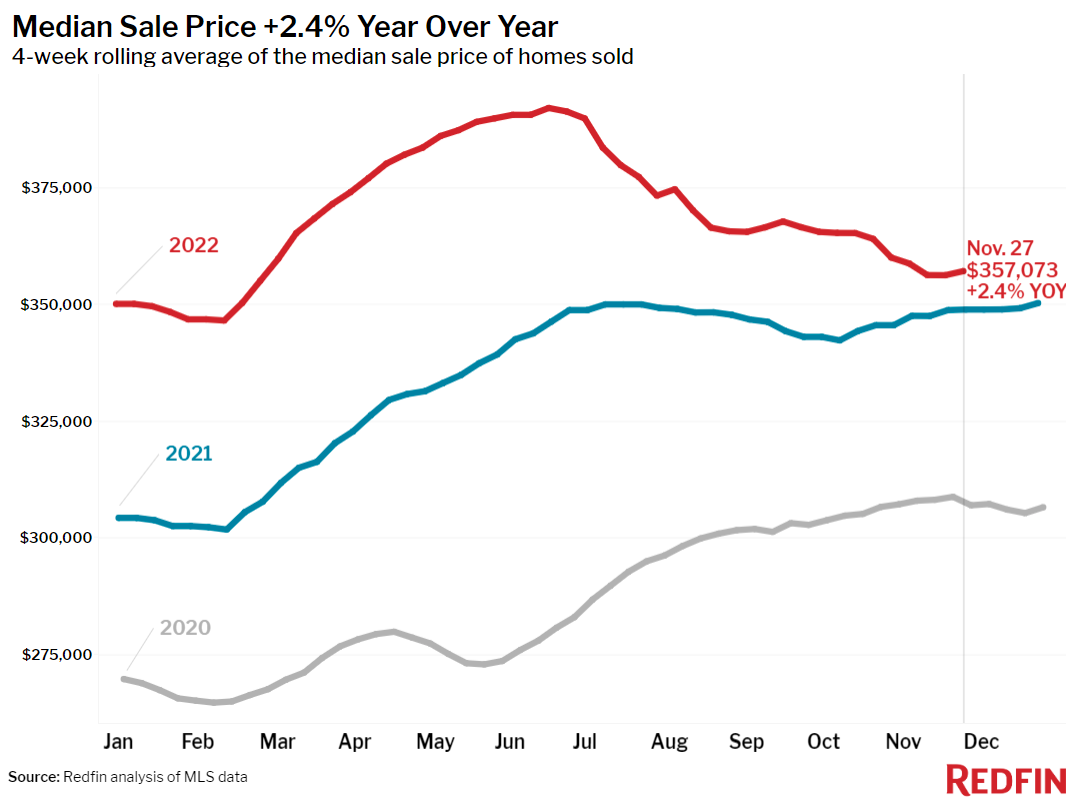

- The median home sale price was $357,073, up slightly from the week before and up 2.4% year over year.

- Among the 50 most populous U.S. metros, pending sales fell the most from a year earlier in Las Vegas (-65%), Phoenix, (-59.7%), Austin (-57.1%), Jacksonville, FL (-54.5%) and Sacramento, CA (-54.2%).

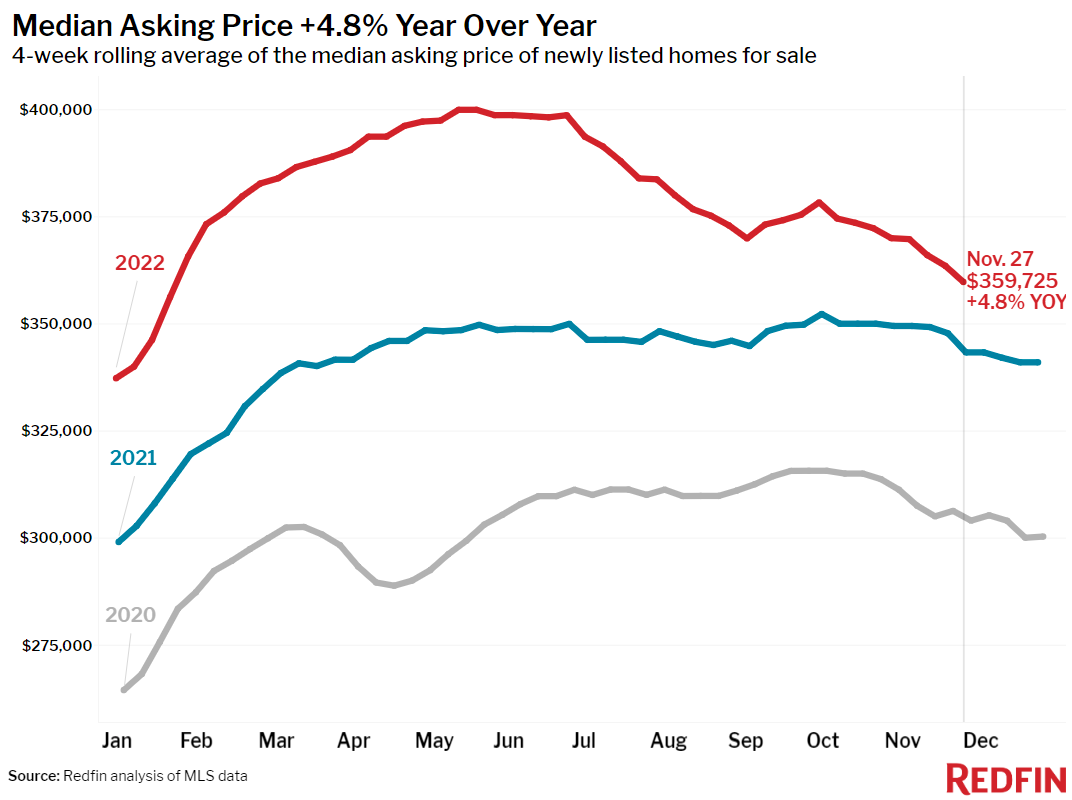

- The median asking price of newly listed homes was $359,725, up 4.8% year over year, one of the slowest growth rates since the beginning of the pandemic.

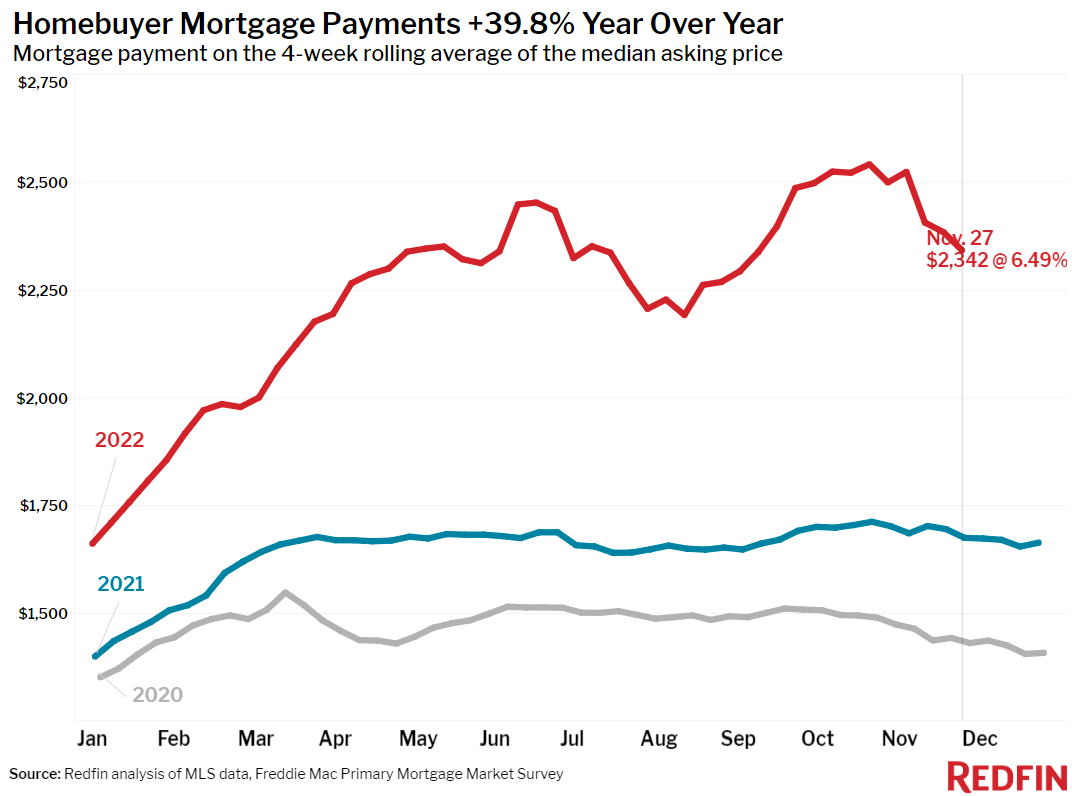

- The monthly mortgage payment on the median-asking-price home was $2,342 at the current 6.49% mortgage rate. That’s down slightly from a week earlier and down 8% from three weeks earlier, when mortgage rates were at 7.08%. Still, monthly mortgage payments are up 40% from a year ago.

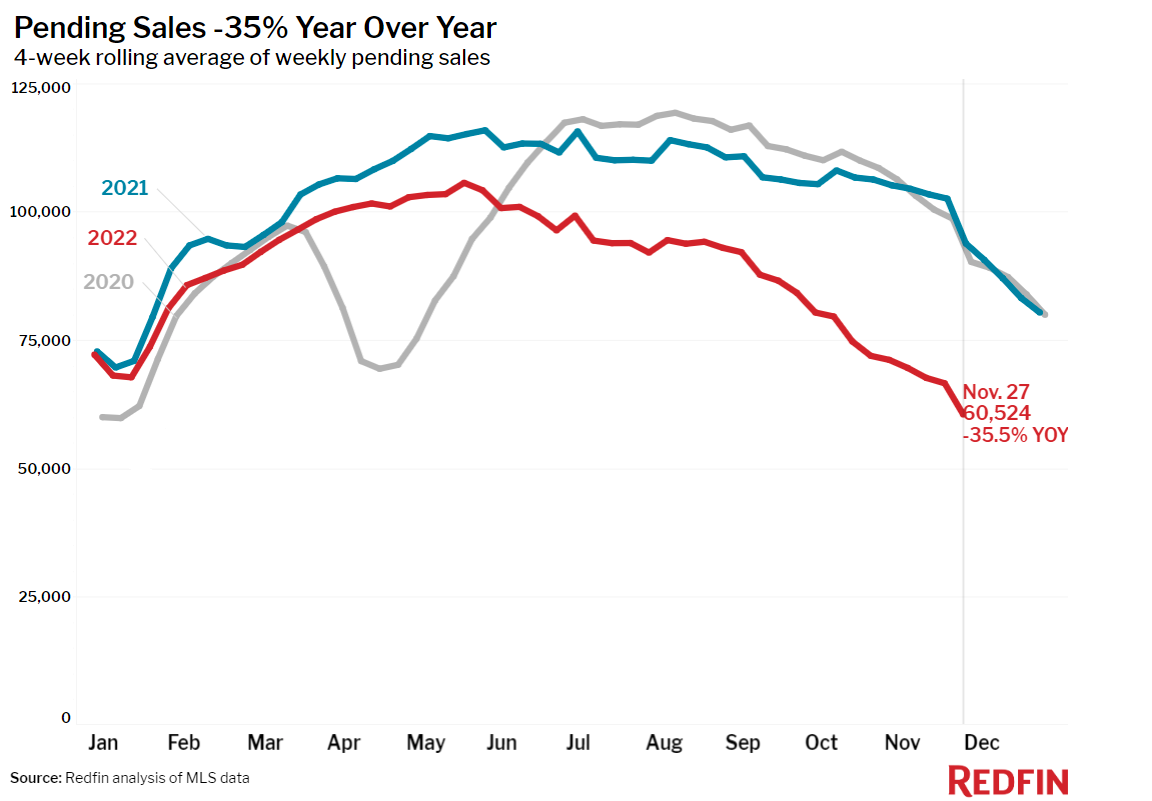

- Pending home sales were down 35.5% year over year, the largest decline since at least January 2015, as far back as this data goes.

- New listings of homes for sale were down 21% from a year earlier, the largest decline since May 2020.

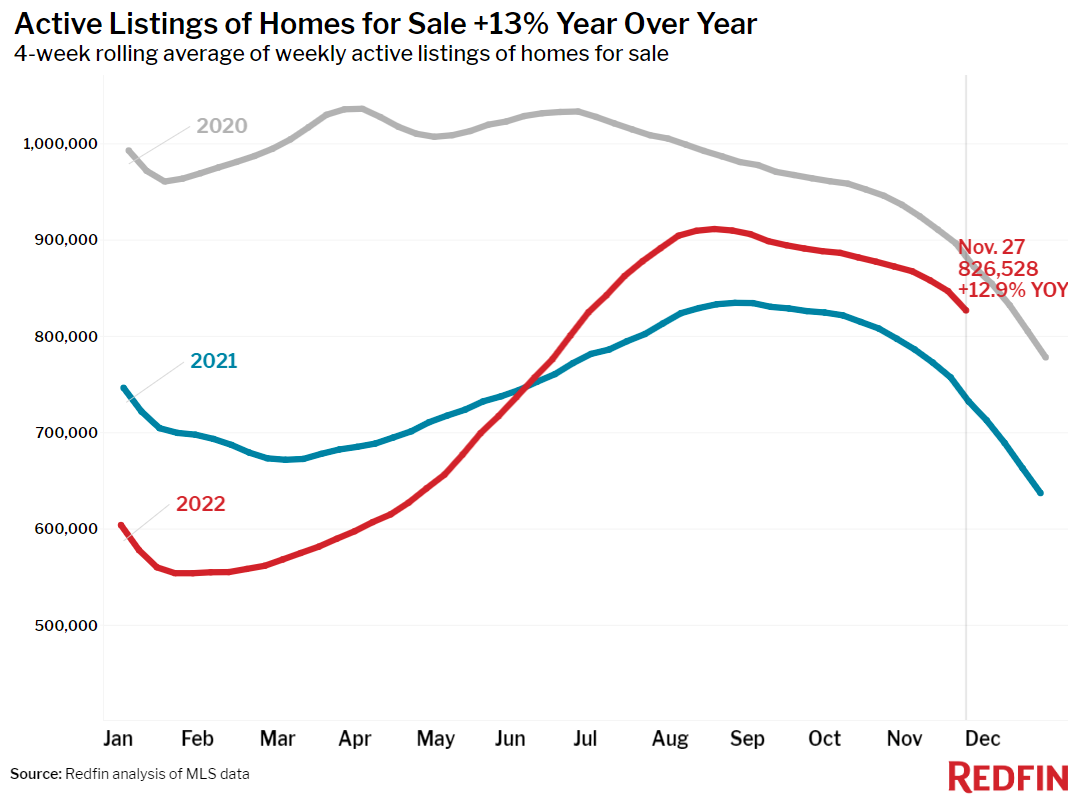

- Active listings (the number of homes listed for sale at any point during the period) were up 12.9% from a year earlier, the biggest annual increase since at least 2015.

- Months of supply—a measure of the balance between supply and demand, calculated by dividing the number of active listings by closed sales—was 4.1 months, up sharply from 3.4 months a week earlier and the highest level since May 2020.

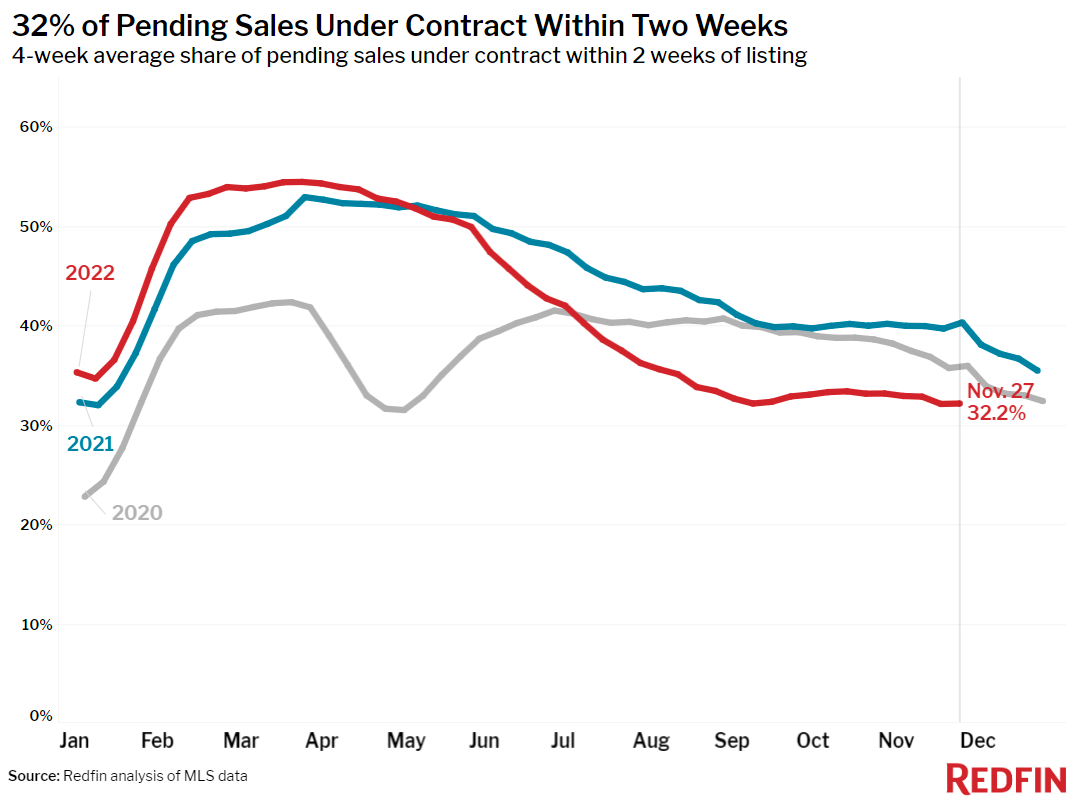

- 32% of homes that went under contract had an accepted offer within the first two weeks on the market, little changed from the prior four-week period but down from 40% a year earlier.

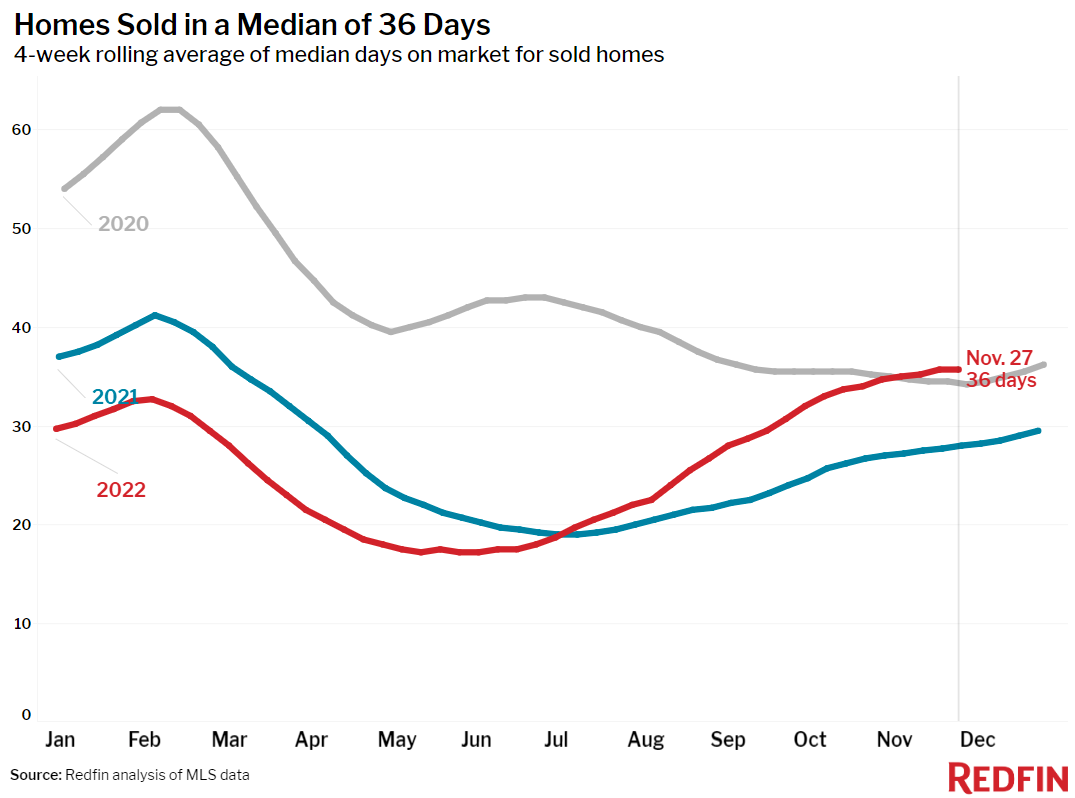

- Homes that sold were on the market for a median of 36 days, up more than a week from 28 days a year earlier and up from the record low of 17 days set in May and early June.

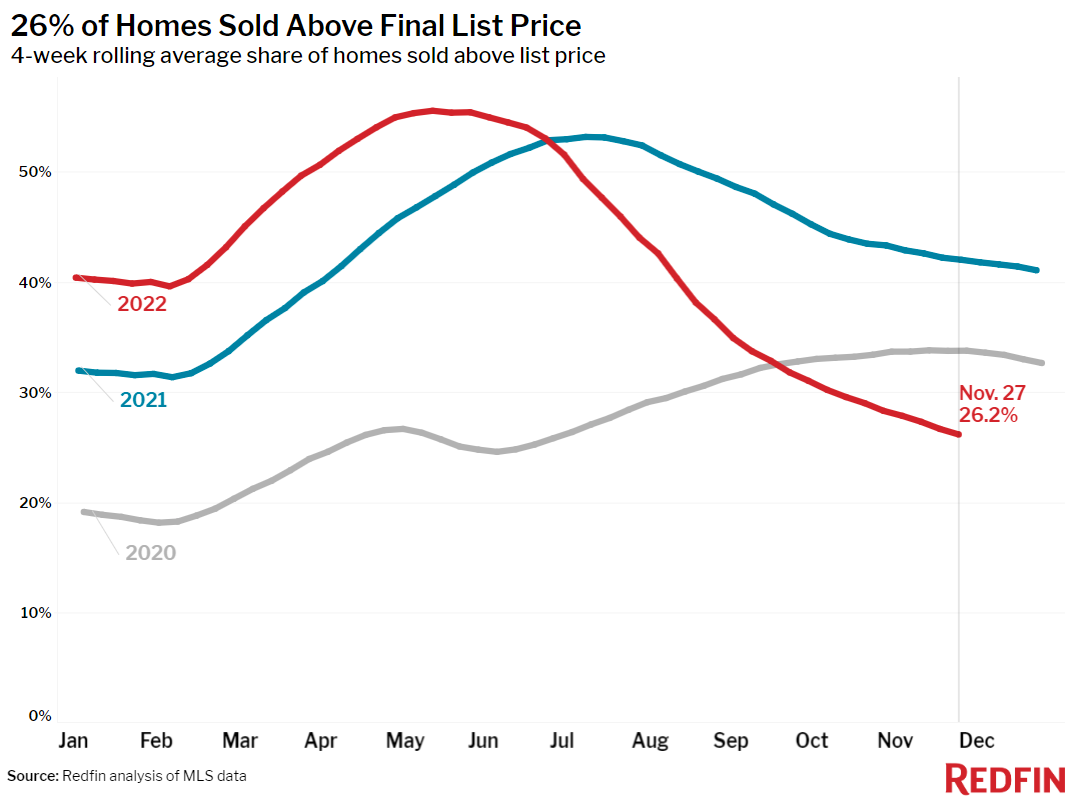

- 26% of homes sold above their final list price, down from 42% a year earlier and the lowest level since June 2020.

- On average, 6.3% of homes for sale each week had a price drop, down sharply from 7.2% a week earlier but up from 2.9% a year earlier.

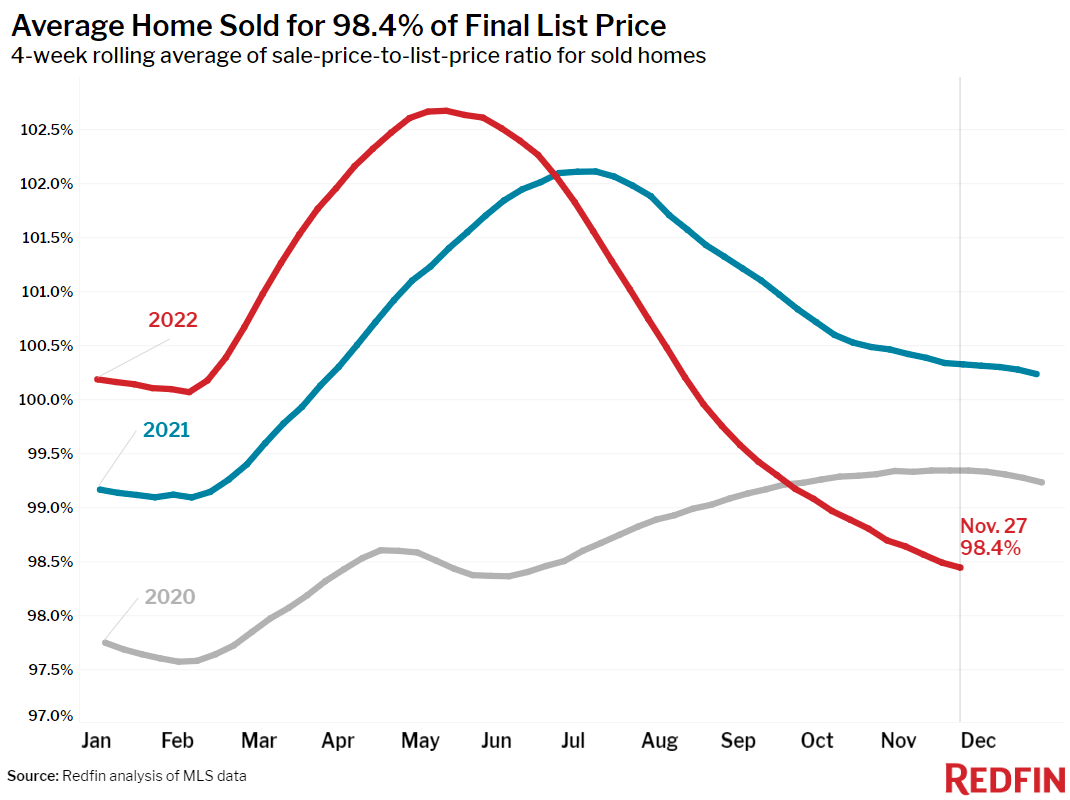

- The average sale-to-list price ratio, which measures how close homes are selling to their final asking prices, fell to 98.4% from 100.3% a year earlier. That’s the lowest level since June 2020.

Refer to our metrics definition page for explanations of all the metrics used in this report.

United States

United States Canada

Canada